What are share classes?

A company issues shares to its various owners (eg founders and investors) to actualise their ownership of part of the company.

Shares are issued with certain specific rights attached to them. Shares might, for example, confer different rights to vote on company decisions, receive dividends, and receive capital.

When a company’s shares have differing rights attached to them, these different types of shares sit within different ‘share classes’.

The types of shares a company is allowed to issue is often determined by the company’s Articles of association and other documents (eg specific Shareholder resolutions that allow a new type of share to be issued).

Classes of shares are usually aligned with specific designated types of share that confer an expected set of rights (eg ‘preference shares’ or ‘ordinary shares’). However, it’s the rights attached to a share that determine its class, rather than its label or ‘designation’.

A particular class of shares that a company has may fit into more than one of the types of shares below. For example, a preference share may be non-voting and redeemable.

Some commonly used share type designations include:

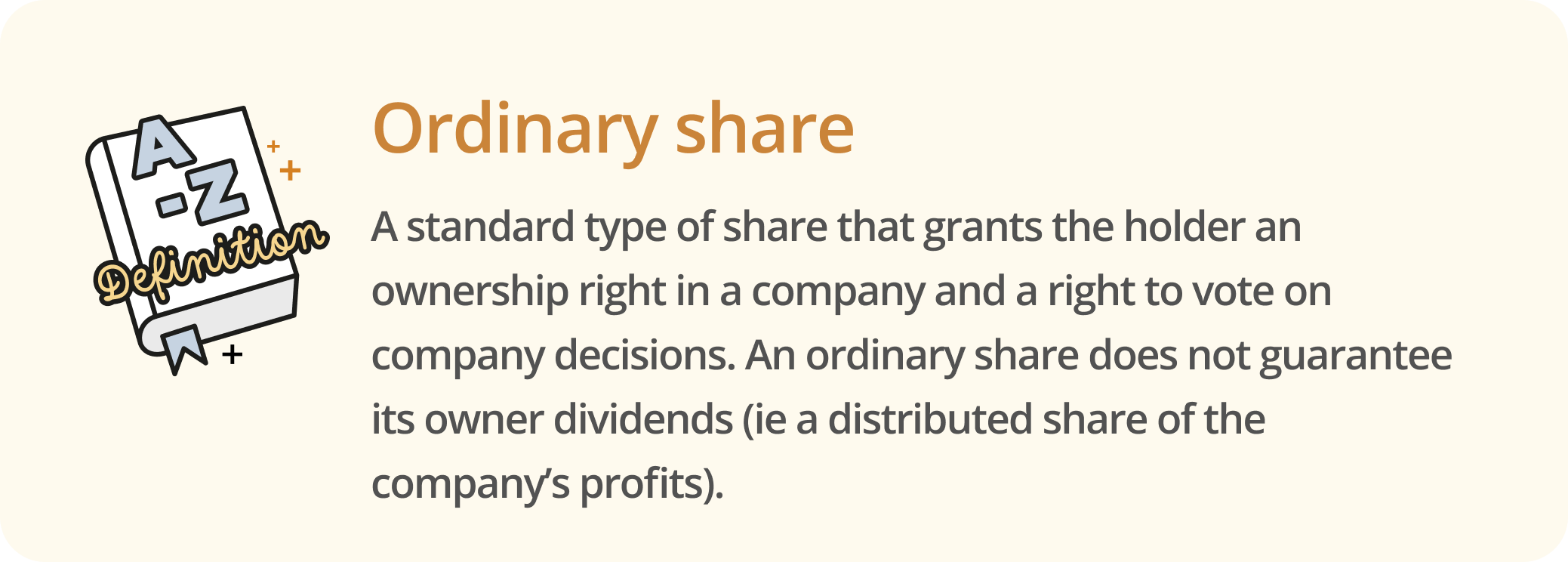

Ordinary shares

Most private limited companies only have one kind of share, called ordinary shares. This is the default share type.

Most private limited companies only have one kind of share, called ordinary shares. This is the default share type.

Ordinary shares generally confer the company’s basic voting rights. Ordinary shares usually give the holder rights to:

-

one vote per share

-

receive an equal dividends entitlement per-share

-

receive part of the distributions from any of the company’s assets in the event of winding up or sale

The rights attached to ordinary shares are generally defined in a company’s Articles of association and/or in the Shareholders’ agreement.

A company will sometimes have multiple classes of ordinary shares that confer different levels of priority regarding voting, dividends, and other rights.

Deferred shares

Deferred shares carry fewer rights than ordinary shares. Their holders are generally last in line behind other shareholders in terms of entitlement to dividends and return of share capital. Deferred shares may not confer voting rights.

Deferred shares can include shares:

-

for which dividends are only paid after dividends for all other classes of shares have been paid

-

for which dividends are only paid after a certain date or event (eg once the company reaches a specified level of profitability)

-

that are not tradable until a certain date – for example, shares issued to employees to give them a long term interest in the company to increase their loyalty

-

which, in the event of insolvency, do not give their holders any rights until all other shareholders are paid

-

shares issued to founders – so that they have a stake in the company, but leave aside more marketable shares with greater rights to use to obtain investment

Non-voting shares

Non-voting shares do not give the holder any voting rights in the company. This means that the holder is entitled to a portion of the company’s capital but is not able to take active part in its general meetings. Non-voting shares are usually equivalent to ordinary shares in all other ways. They offer a method of diversifying and growing company ownership whilst maintaining control of decision making, by restricting voting rights to certain shareholders.

Non-voting shares are often issued to employees or to family members of the main shareholders. This class of shares allows the main shareholders to retain control of the company whilst multiplying the number of shareholders.

Redeemable shares

Redeemable shares are shares that can be bought back by the company at some point in the future. The terms of specific redeemable shares can vary, for example by:

-

the redemption date (ie when the shares can be redeemed) – this can either be fixed in advance (eg at three years from the date the share is issued or on the happening of some specific event) or left to the parties’ discretion

-

the redemption price (or ‘call price’) – this is set when the shares are issued (either as a number or by reference to a set method of determining price). It’s often the same as the issue price, but not necessarily

-

who can redeem – the company, the shareholder, or both may be given the option to redeem

The ability to redeem shares is limited and is subject to specific statutory requirements. Private companies can only issue redeemable shares if doing so is not restricted by its articles of association.

Share redemptions are similar to share buybacks, but have advantages such as not requiring the payment of stamp duty as would be required during a buyback.

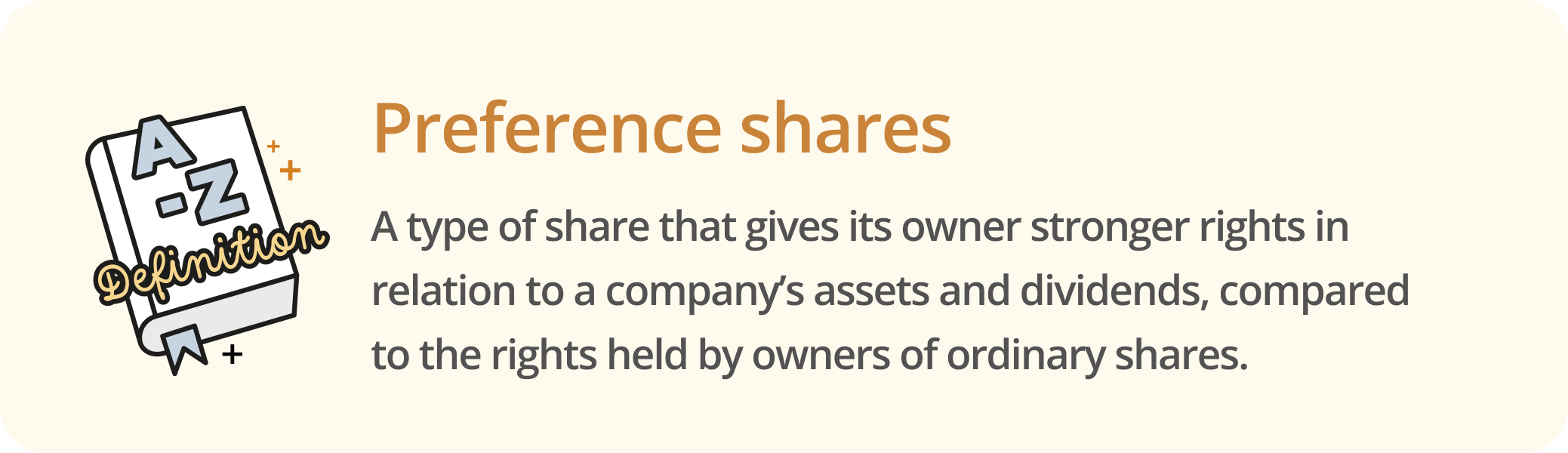

Preference shares

Preference shares give their holders preferential (ie stronger, priority) rights in comparison to those held by ordinary shareholders. This can include preferential rights in relation to dividends (eg they may receive dividends ahead of ordinary shareholders), capital returns (eg by having a higher priority claim to the company’s assets in case of insolvency), or both of these. It’s common for either dividends or capital that the shareholder is entitled to receive with priority to have a fixed amount.

As preference shares carry many benefits and guarantees, they’re mostly issued to investors, for example, venture capitalists.

Preferred shareholders often hold weaker ownership rights in a company than other (eg ordinary) shareholders. For example, preference shares are often non-voting and sometimes redeemable.

Redeemable preference shares are a common way of financing a business. They allow a company to repurchase its shares in the future (eg if interest rates fall and the company wants to issue new shares with a lower dividend rate) while giving investors the possibility to get their money back at a pre-agreed price

Management shares

Management shares are simply shares held by company management. They’re generally created to give their holders extra voting rights at company meetings (eg two votes for each share rather than one). These shares are often used to help company directors to retain control of a company when shares are issued to outside investors.

Alphabet shares

Alphabet shares are a subclass of ordinary shares that differ in some way to the company’s other ordinary shares. Creating alphabet shares helps a company to vary the rights granted to different shareholders.

They’re called alphabet shares as companies commonly have various share classes labelled with alphabet letters (eg A, B, C, D, and so on depending on the number of classes created). Each of these classes will confer different rights, for example, voting rights, rights to dividends, and rights to capital.

Naming classes of shares alphabetically is an alternative used instead or as well as naming share classes descriptively (eg as non-voting shares, preference shares, or redeemable shares).

Utilising alphabet shares enables companies to enhance or restrict certain shareholders’ rights. For example, ‘A shares’ can have a greater rate of dividend payments than ‘B shares’ so that, for the same number of shares, owners of A shares receive more than owners of B shares.

Why are there different types of shares?

Having multiple classes of shares can help a company to:

-

attract investors (eg by making some shares particularly valuable)

-

push dividend income into a certain direction

-

remove or enhance the voting powers of certain shareholders

-

motivate staff to remain with the company (eg through employee share schemes)

Having different share types also helps differentiate easily between the different powers held by different groups of shareholders. For example, to clearly establish who has rights to:

-

attend general meetings

-

vote on company resolutions

-

receive dividend payments

-

participate in capital distribution on winding-up of the company

Ask a lawyer if you need help deciding which classes of shares to issue or help issuing shares.