What is bookkeeping?

Bookkeeping is the essential, day-to-day process of recording all your business's financial transactions. Think of it as creating and maintaining the financial diary of your business. This involves accurately tracking every penny that comes in and goes out.

The main tasks of bookkeeping include:

-

recording sales, purchases, payments, and receipts

-

issuing invoices to customers and chasing payments

-

processing payroll for any employees

-

reconciling your business bank accounts to ensure your records match the bank's records

-

managing Value Added Tax (VAT) records if your business is VAT-registered

-

keeping digital records and submitting quarterly updates to HMRC if you are required to comply with Making Tax Digital (see below)

Whether you're a sole trader, in a partnership, or run a limited company, you must keep accurate and up-to-date records. Good bookkeeping is the foundation of your tax returns, whether that’s a Self Assessment tax return for a sole trader or a Company Tax Return for a limited company.

What is accounting?

Accounting is a higher-level process that uses the organised data from your bookkeeping records to give you a clear picture of your business's financial health. If bookkeeping is the diary, accounting is the story it tells. An accountant (or you, if you manage your own accounts) will analyse, interpret, and summarise this financial data.

The main tasks of accounting include:

-

preparing financial statements - this includes the profit and loss account (which shows your income and expenses over a period) and the balance sheet (a snapshot of your assets and liabilities at a specific point in time)

-

filing tax returns - accountants use the financial records to prepare and file the correct tax returns with HMRC. This includes the Self Assessment tax return for sole traders and partners, the Partnership Tax Return, and the Company Tax Return and corporation tax calculations for limited companies

-

financial analysis and planning - accounting involves analysing financial performance to help you make strategic business decisions, create budgets and forecasts, and ensure legal compliance

-

auditing - for larger companies, accounting includes auditing the financial records to ensure they are accurate and comply with the law

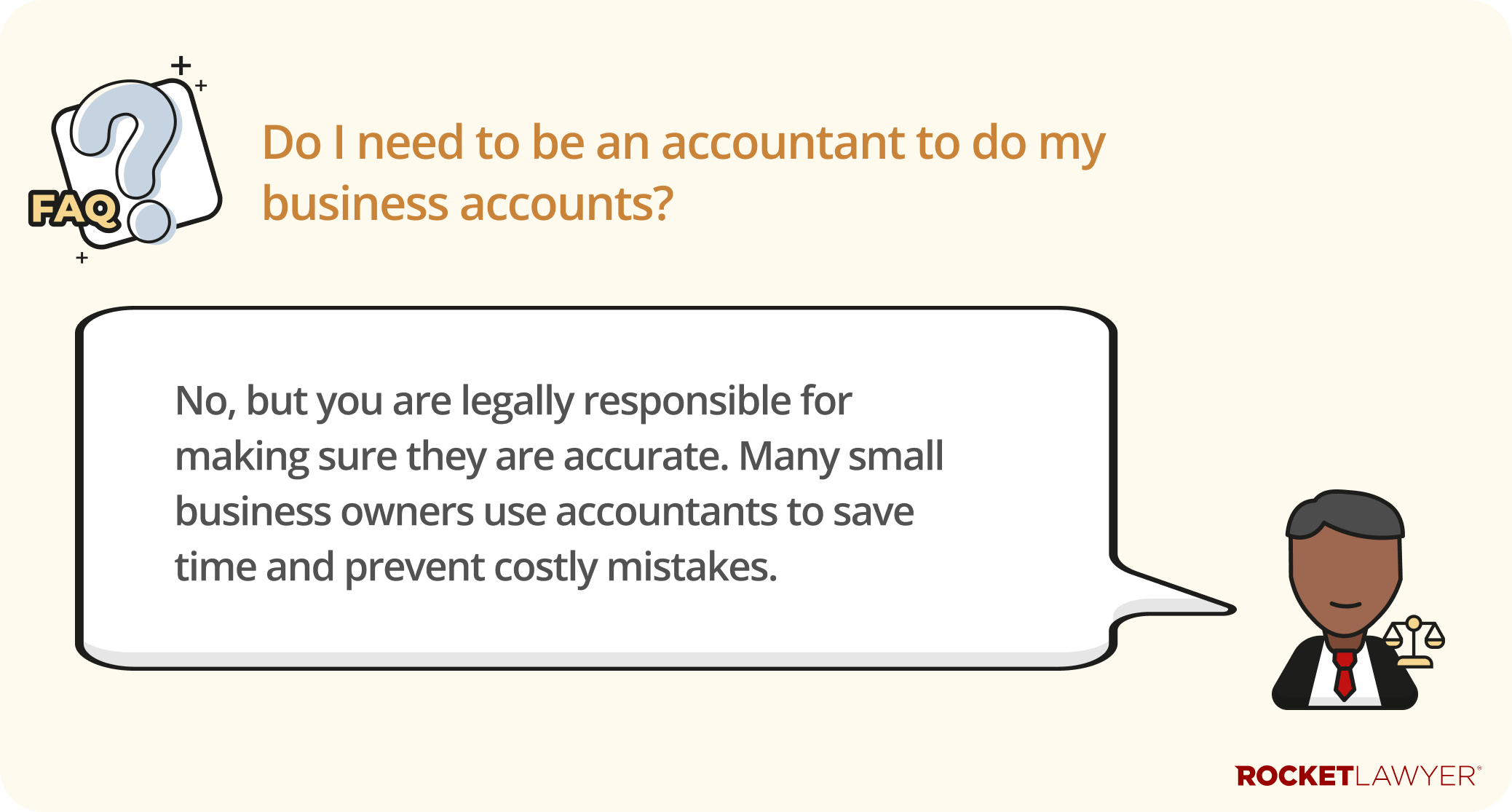

While anyone can do their own bookkeeping, many business owners hire an accountant for these more complex tasks to ensure they meet all their legal obligations with Companies House and HMRC, and to get expert financial advice.

What financial records must my business keep?

All businesses in the UK must keep detailed financial and accounting records. These records are crucial not just for managing your business, but also for meeting your legal obligations. HMRC may wish to inspect your records at any time to check that you're paying the right amount of tax, that your staff are being paid correctly, and that National Insurance contributions are being properly made. They also check records to ensure the business is not being used for illegal activities like money laundering.

The specific records you need to keep vary depending on your business structure.

For sole traders and partnerships

If you're a sole trader or in a business partnership, you must keep records of:

-

all your business sales and income

-

all your business expenses

-

VAT records if you’re registered for VAT

-

PAYE records if you employ people (eg details of payments to employees and deductions)

-

records of your personal income

-

any money you’ve invested in the business or taken out for personal use

These records are essential for completing your annual Self Assessment tax return.

If you are required to comply with Making Tax Digital for income tax, these records must be kept digitally using HMRC-compatible software (more on this below).

For limited companies and LLPs

Limited companies and limited liability partnerships (LLPs) have more formal record-keeping and reporting requirements because they are legally separate from their owners.

In addition to all the records mentioned for sole traders (sales, expenses, VAT, PAYE), you must also keep:

-

details of assets owned by the businesses (eg buildings or machinery)

-

details of liabilities (ie money the company owes)

-

records of stock the business owns at the end of each financial year

-

any other financial records needed to prepare and file your annual accounts and Company Tax Return

Why is the way I keep records important?

The key to good record-keeping is permanence. You shouldn't keep business records in a format where they can be easily changed or deleted without a trace. This is why many businesses use accounting software that creates a secure, unalterable log.

All accounting rules are based on a simple system:

-

record transactions as they happen

-

classify and reconcile those transactions to show what the business has received and spent

-

use these records to see if the business has made a profit during an accounting period

If your records show that your business has made a profit, you may have to pay tax on it. Without permanent and accurate records, it's impossible to do this correctly.

How long do I need to keep business records?

The rules on how long you must keep records depend on your business structure:

-

sole traders and partnerships - you must keep records for at least five years after the 31 January submission deadline of the relevant tax year

-

limited companies - you must keep accounting records for at least six years from the end of the last financial year they relate to

HMRC can issue penalties if your records aren't accurate, complete, and readable, so it's vital to have a good system in place.

What is Making Tax Digital?

What is Making Tax Digital?

Making Tax Digital (MTD) is HMRC's programme to modernise the tax system by requiring businesses and individuals to keep digital records and submit tax information electronically.

MTD for income tax came into force on 6 April 2026 for sole traders and landlords with qualifying income over £50,000. Qualifying income is your gross income from self-employment and/or UK property before expenses are deducted. It does not include employment income, pension income, or dividends.

If you fall into this category, you must:

-

keep digital records of your income and expenses using MTD-compatible software

-

submit quarterly updates to HMRC summarising your income and expenses

-

submit a final end-of-period statement at the end of the tax year

The income threshold will reduce to £30,000 from April 2027, and to £20,000 from April 2028, bringing more sole traders and landlords into scope over time.

MTD for corporation tax is expected to be introduced for limited companies in the future, although an exact date has not yet been confirmed by HMRC.

For more information, see the government’s guidance on MTD for income tax. If you are unsure whether MTD applies to your business, you should speak to an accountant.

If you have any questions about your business's financial responsibilities, do not hesitate to Ask a lawyer.